Maximizing College Savings with a 529 Plan

Saving for college can feel overwhelming, but a 529 savings plan offers a tax-advantaged way to invest in a child’s future education. Whether you’re a parent, grandparent, or guardian, understanding how a 529 plan works can help you maximize savings while reducing the financial burden of higher education.

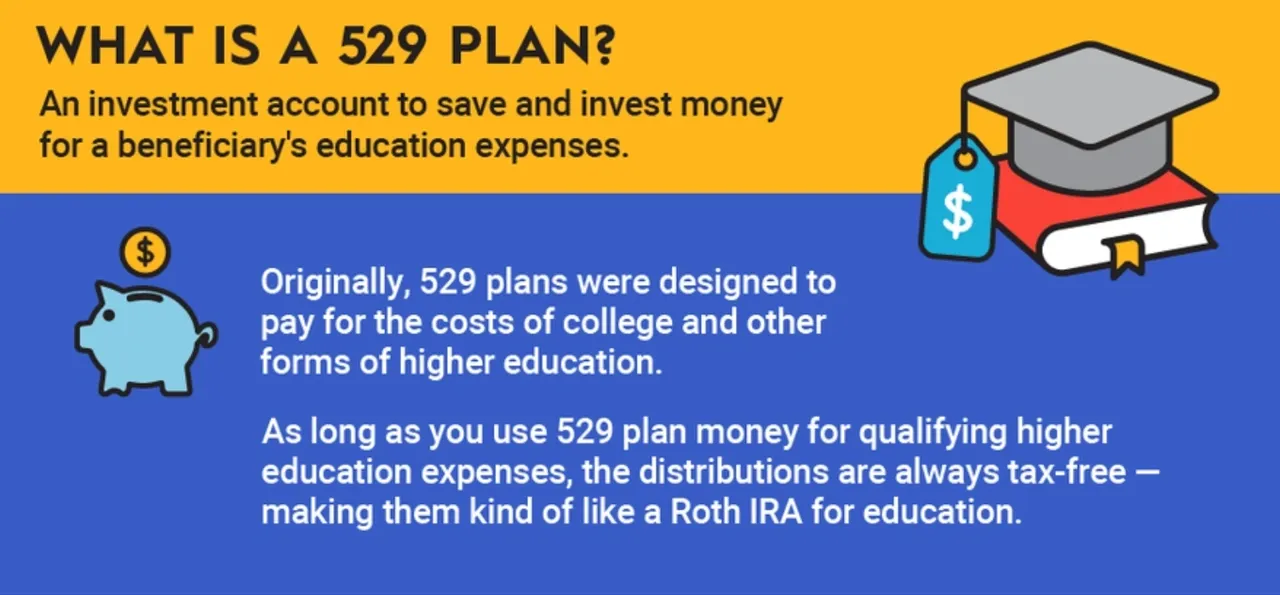

What is a 529 Plan?

A 529 plan is a tax-advantaged investment account designed specifically for education expenses. These plans are sponsored by states, state agencies, or educational institutions, and they offer two main types:

- College Savings Plans – These allow funds to grow tax-free when used for qualified education expenses.

- Prepaid Tuition Plans – These let you prepay tuition at today’s rates for participating colleges and universities.

Tax Benefits of a 529 Plan

One of the biggest advantages of a 529 plan is its tax benefits:

- Tax-Free Growth – Earnings in a 529 plan grow tax-free, meaning you won’t pay federal taxes on investment gains if used for qualified expenses.

- Tax-Free Withdrawals – Withdrawals are tax-free when used for eligible education costs, including tuition, books, supplies, and room & board.

- State Tax Deductions – Many states offer deductions or tax credits for contributions to a 529 plan, making it even more beneficial.

What Expenses Qualify for a 529 Plan?

Funds from a 529 plan can be used for:

- Tuition and fees at eligible colleges, universities, and trade schools.

- Room and board for students enrolled at least half-time.

- Books and supplies required for courses.

- Computers, software, and internet access needed for schoolwork.

- K-12 tuition (up to $10,000 per year per student at private or religious schools).

- Student loan repayments (up to $10,000 lifetime limit per beneficiary).

Who Can Open a 529 Plan?

Anyone can open a 529 plan for a designated beneficiary, including parents, grandparents, relatives, or even the student themselves. There are no income limits, and the funds can be transferred to another family member if the original beneficiary doesn’t use them.

How Much Can You Contribute?

While contribution limits vary by state, most plans allow you to contribute over $300,000 per beneficiary. However, contributions are considered gifts for tax purposes, meaning amounts over $18,000 per year (in 2024) may count toward your lifetime gift tax exemption.

529 Plan vs. Other College Savings Options

- Custodial Accounts (UGMA/UTMA) – These accounts give children full control of funds at adulthood, whereas 529 plans remain under the account holder’s control.

- Coverdell ESAs – While also tax-advantaged, they have a $2,000 annual contribution limit and income restrictions.

- Savings Accounts – Unlike traditional savings accounts, a 529 plan allows for greater growth potential with tax-free earnings.

What If the Beneficiary Doesn’t Go to College?

If the designated beneficiary doesn’t use the funds, you have options:

- Change the beneficiary to a sibling or another family member.

- Save the funds for future education (many plans have no age limit).

- Withdraw the funds (subject to income tax and a 10% penalty on earnings for non-qualified withdrawals).

Final Thoughts

A 529 savings plan is one of the best ways to prepare for future education costs while enjoying valuable tax benefits. Whether you’re saving for your child’s college tuition or planning ahead for K-12 expenses, a 529 plan offers flexibility, growth potential, and long-term financial advantages.

If you’re ready to start saving for college, talk to a financial professional to choose the best 529 plan for your needs!

Leave a Reply